ACCIDENTAL & SAVINGS X LIFE INSURANCE

How Wysh grew their ARR via product expansions

Life Insurance

Product Management

Strategy

TOTAL REDUCTION IN CUSTOMER ACQUISITION COST (CAC)

TOTAL REDUCTION IN CUSTOMER ACQUISITION COST (CAC)

44%

ADDITIONAL COVERAGE

ISSUED*

ADDITIONAL COVERAGE

ISSUED*

$100M

NUMBER OF

UNIQUE CUSTOMERS

1.5M

UNDERWRITING

ACCEPTANCE RATE

UNDERWRITING

ACCEPTANCE RATE

68%

*6 MONTHS AFTER

MVP LAUNCH

*6 MONTHS AFTER

MVP LAUNCH

FINTECH

AWARDS

excellent

4.5/5

180 REVIEWS

⭐ About Wysh’s Embedded Term Life & Savings Product & Accidental Death Insurance Product

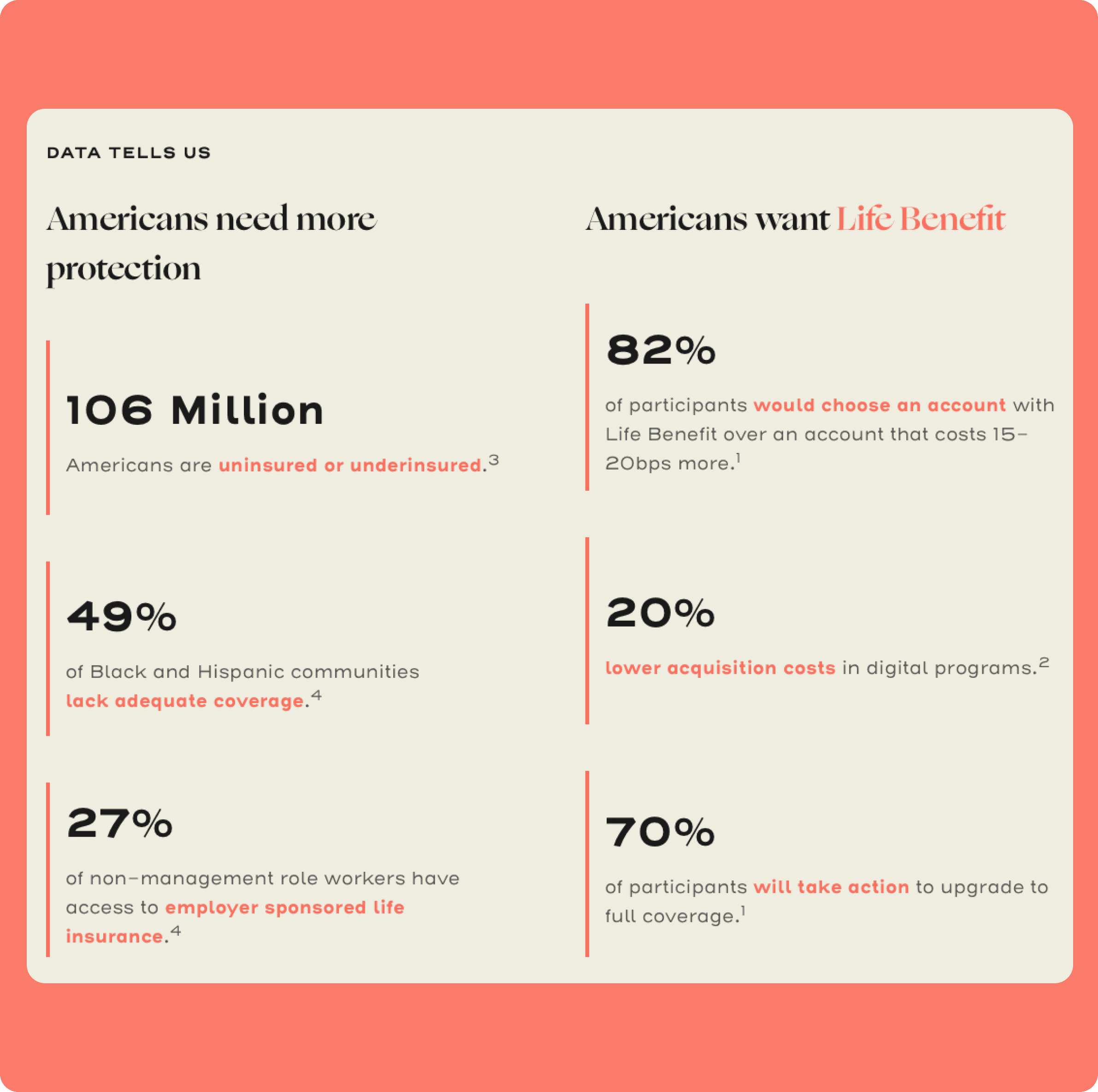

Even with consistent user improvements to our core Term Life Insurance Product, Wysh still had an extremely high Customer Acquisition Cost (CAC) at $2500. There was no way to bring in users into the purchase funnel, especially users who aren’t actively thinking of life insurance - much less being able to acquisition those customers. Due to this - an out-of-the-box solution was required.

Even with consistent user improvements to our core Term Life Insurance Product, Wysh still had an extremely high Customer Acquisition Cost (CAC) at $2500. There was no way to bring in users into the purchase funnel, especially users who aren’t actively thinking of life insurance - much less being able to acquisition those customers. Due to this - an out-of-the-box solution was required.

🚧 Project Background

🚧 Project Background

Upon launch of our Term Life Insurance Product, we only reached a 40% underwriting acceptance. This was extremely below industry standard which is approximately 60%. That’s a significant gap. But we realized why the delta existed -

1. Our marketing was bringing in unhealthy users. Certain demographic data such as region & income could be filtered for better candidates top-funnel.

2. Since we’re only digitally underwritten (no medical exams) - a significant number of users were rejected due to this.

3. Rejected users were lost customers. There was nothing we could offer them.

Upon launch of our Term Life Insurance Product, we only reached a 40% underwriting acceptance. This was extremely below industry standard which is approximately 60%. That’s a significant gap. But we realized why the delta existed -

1. Our marketing was bringing in unhealthy users. Certain demographic data such as region & income could be filtered for better candidates top-funnel.

2. Since we’re only digitally underwritten (no medical exams) - a significant number of users were rejected due to this.

3. Rejected users were lost customers. There was nothing we could offer them.

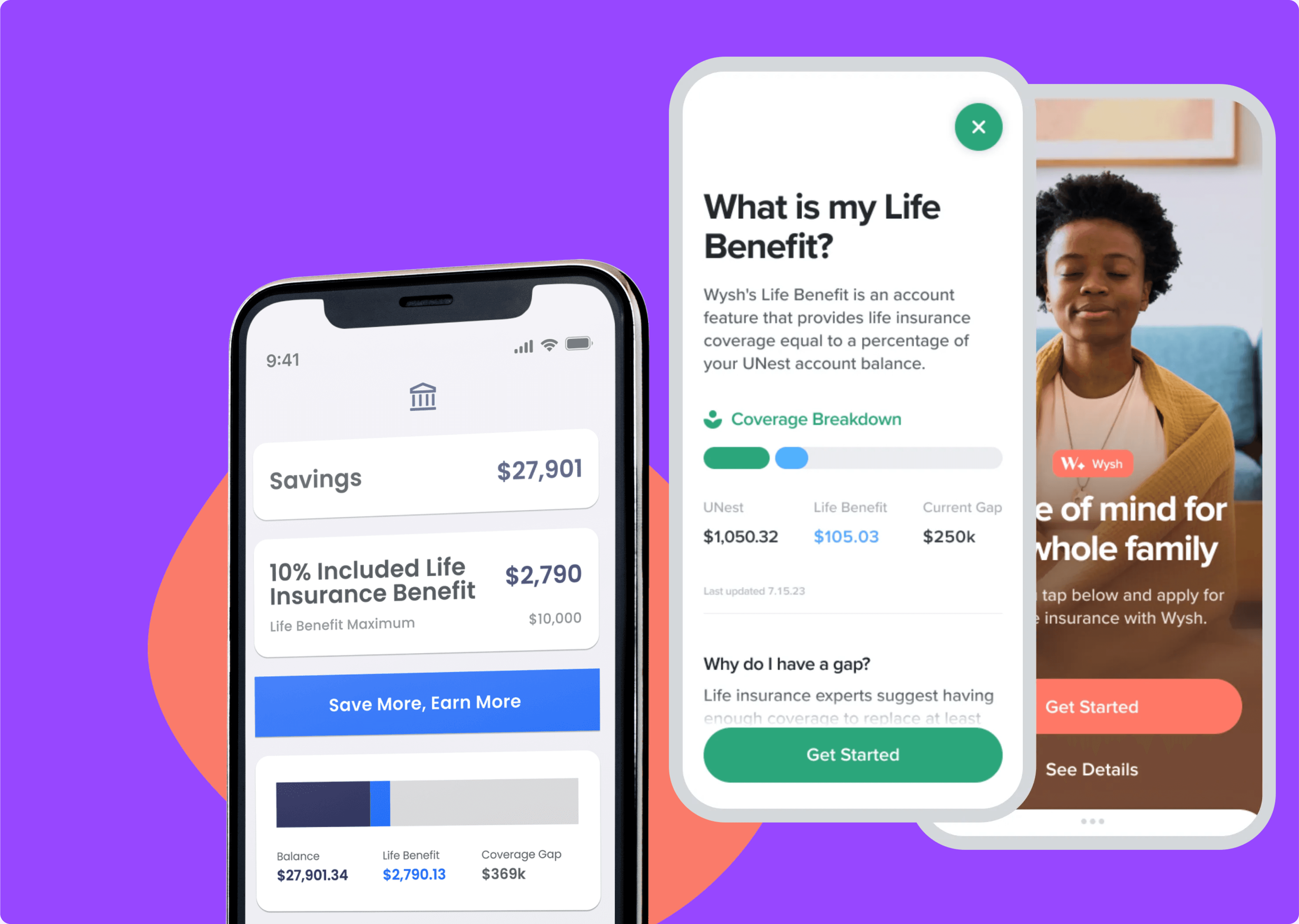

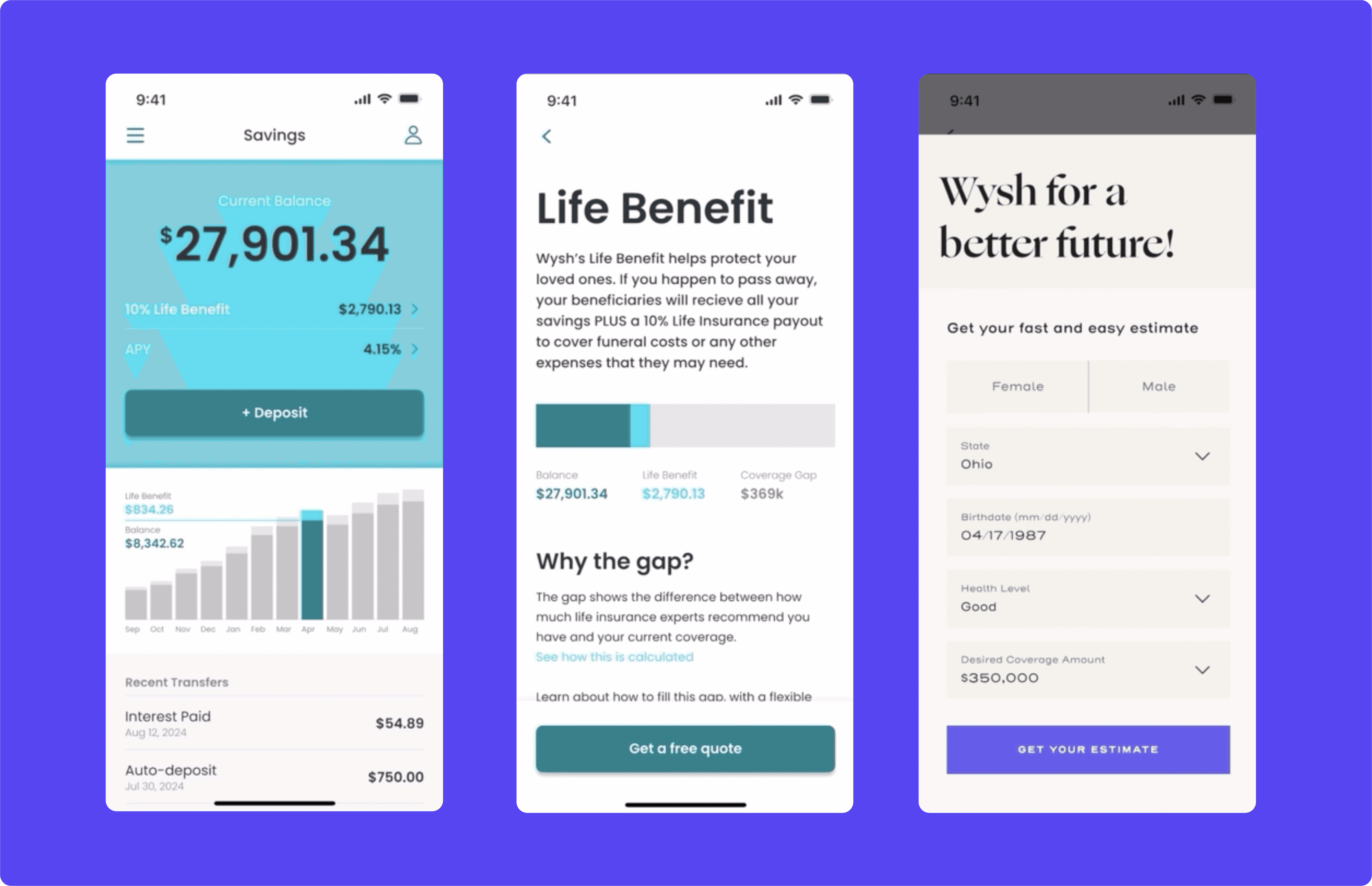

🏦 Embedded Savings x Term Life Insurance: 80% of Americans have a savings account, but only 50% of Americans have life insurance. That’s a massive financial gap. Banks are trying to compete on high APY offerings to acquisition customers, however the benefits gets lost within a sea of the same. So why not acquisition those customers by offering a unique benefit such as life insurance, so that coverage is top-of-mind for them. When they reach a life milestone they can easily purchase term life insurance through Wysh.

⚠️☠️ Accidental Death Insurance: Not everyone is going to be accepted for term life insurance, with health conditions, extreme smoking habits or for other risky behavior. An alternative solution to “bad health” candidates or candidates with extremely high premiums -- is accidental death insurance. Basically an insurance that pays out your coverage if you were to die but accident. People don’t tend to realize - that among young healthy people, an accident is the most common way a person can die. So having certain protection is better than nothing at all.

🏦 Embedded Savings x Term Life Insurance: 80% of Americans have a savings account, but only 50% of Americans have life insurance. That’s a massive financial gap. Banks are trying to compete on high APY offerings to acquisition customers, however the benefits gets lost within a sea of the same. So why not acquisition those customers by offering a unique benefit such as life insurance, so that coverage is top-of-mind for them. When they reach a life milestone they can easily purchase term life insurance through Wysh.

⚠️☠️ Accidental Death Insurance: Not everyone is going to be accepted for term life insurance, with health conditions, extreme smoking habits or for other risky behavior. An alternative solution to “bad health” candidates or candidates with extremely high premiums -- is accidental death insurance. Basically an insurance that pays out your coverage if you were to die but accident. People don’t tend to realize - that among young healthy people, an accident is the most common way a person can die. So having certain protection is better than nothing at all.

Growing Partnerships

Growing Partnerships

Since Life Benefits launch in 2022 - Wysh has enabled over 5 integrations. This includes banks, credit unions, an investment account providers and more!

Since Life Benefits launch in 2022 - Wysh has enabled over 5 integrations. This includes banks, credit unions, an investment account providers and more!